Everything you need to know about Luxury – but were afraid to ask

Always bear in mind that whilst no-one actually needs Luxury, most of us want it, this is what drives its universal appeal, and explains perhaps the paradox of the citizens of the world’s dominant Communist country being its greatest consumers today. You can set rules (in China it’s about visibility) but the appetite is real and eternal (from the purple dye, spices and silks of the patricians of the ancient world to the exotic leather handbags and complicated watches of today, the thread is always the same). One way or another, we all seek validation in some form.

So what is a Luxury Good or indeed a Luxury Experience? In my view the definition of Luxury entails:

- Desireability

- Scarcity (ideally Exclusivity but that is rare these days)

- A sense of Status, essentially Wealth Signalling

- Quality and Craftsmanship, or at least it should

The Luxury Industry as we know it is essentially 35 years old I think, it was way too niche and small before 1990. It has grown enormously since as part of the ‘premiumisation’ of everything as I call it.

Luxury was for the very few, this is no longer the case.

The aggregate Sector revenues were €63bn in 1994 (when I started looking at it), they were €375bn last year. Furthermore, before Covid the sustainable organic growth was 6% each year, more dynamic than any other consumer segment. First the mature markets, then China, then the emerging markets, as it evolved everyone wanted a piece of this and whilst the total spend multiplied over 4x, the spend from developing economies multiplied over 20x in the same period.

Momentum went wild with Covid: -22% in 2020 then +29% in 2021 closing the year bigger than it was in 2019. And it kept growing as we were all a bit bored with money to spend as there was not much we could do (well, except for Sweden, you guys were smarter), this was the time when people spent a lot to ‘buy’ things, +73% in 3 years between 21-23 or 3x normal growth. Too fast, too much.

Of course this is the end created a problem, too much volume and too much price. Not all brands went a bit mad but many did, Dior revenues went from €2.2bn to €10bn in less than five years! A lot of stores opened and a lot of product was being sold, scarcity went out of the window for some. This means all worked well until it no longer did, and in 2024 we saw a marked shift when people spent more ‘to experience moments’ than ‘to buy things’. The industry of Luxury ‘things’ suddenly flatlined which was absolutely inevitable given these excesses.

Annons

What has happened since ?

2025 was a wasted year due to the US administration’s erratic policies although it became clear by the Autumn that tariff impact would be less than feared, and the ‘things’ sector showed signs of life again.

Indeed 2026 started rather well on about +6% (or back to normal and more reasonable growth), then we had a war in the Middle East and volatility was back, but only to a point as we have seen growth so far this year in spite of this, indicating more resilience than many thought.

So who or where or indeed what is doing well at the moment (remember, trends vary a lot now by market, nationality and category)?

By market Korea and the US are strong, China is finally gradually recovering from its excesses, but Europe is still a problem (fewer tourists from Asia, remember in Europe visitors are almost 60% of Luxury sales) and the Middle East obviously down a lot.

By nationality the Koreans and the Americans are strong as well as some of the Japanese and the Middle East cluster (they just buy elsewhere but not so much in Dubai etc) with the Europeans still a bit weak.

By category jewellery has done well, better than leather goods so far (jewellery grew a lot less in 2021-23) whilst watches are either strong or weak by brand (eg Rolex good, Omega not so much etc).

By brand the strong performers are at the top (think Ferrari, Cucinelli, Loro Piana, The Row, Chanel etc) and at the bottom (Ralph Lauren, Golden Goose, Coach, Swedish brand Toteme too). Few do well in the middle these days.

Perhaps it is important to highlight and remember that Luxury demand, in evolving, has changed and essentially bifurcated with the top end doing rather well but the middle struggling. Visualise who buys Luxury by levels of wealth, the wealthy have always spent more every year, and for some brands they account for 75% of their sales.

Think about it this way: the buyers of Luxury are divided in three types: the very wealthy, the wealthy and the middle class/aspirational buyers. The first two are doing well, the last segment is suffering and has been since 2024. These are the customers most hit by interest rates, inflation, mortgages etc, you would expect a lot more volatility here. So 2/3 of Luxury spend is growing, 1/3 has shrunk. Overall though, we are starting to grow again.

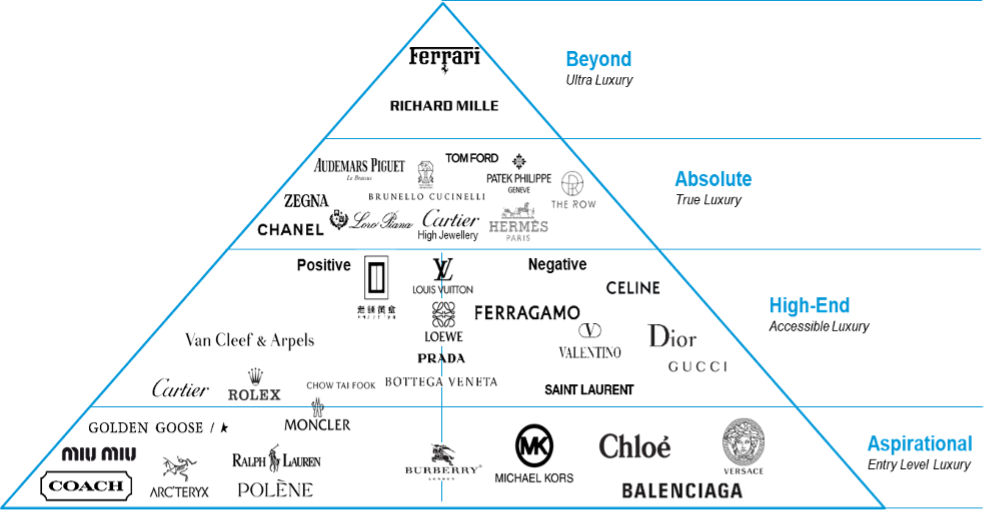

Here is my version of the Luxury Pyramid for many of the famous names, any brand can be placed in here.

The segmentation represents not the perception of the brand itself, but the characteristics of its customers. Put it simply: the higher up, the better. Wealthier, less volatile, more loyal.

When you look at the brands, it is those that aim for the top that are doing rather better and as you move into the aspirational space at the bottom the difference between the superstars (eg Coach) and the weak names (eg Michael Kors) is very obvious. I think this difference in momentum will gradually drop over time but today it has become the dominant feature.

So we have a Sector that is gradually recovering but is still patchy with a lot of good and bad areas, I think we will see growth this year but magnitude depends on the chaos in the Persian Gulf so it is difficult to quantify a number at this time. What we do know is that there are brands that are growing double-digit and some others that continue to see market share erosion. I continue to believe that any signs of geopolitical stabilisation will see a very rapid recovery in trends globally and we can return to normal levels of growth quickly.

Remember: 6% annual growth is doubling in 12 years, that would add almost €400bn in spend.

All that said, now think of the Luxury customers and we already mentioned the difference between buying things and doing things/paying for unique moments and memories and experiences, they indeed have been spending more than ever as they enjoy living Luxury Experiences, think elite holidays, Luxury cruises, health and wellness and such like. This element of Luxury has been on fire, growing double digits every year since 2021. I think this will slow down a little over time but it remains very dynamic and really is part of the consumption of Luxury overall like never before.

This matters: the €375bn I mentioned earlier refers to Luxury goods alone, the bags, the watches, the shoes, add to that the cars, the travel, the events, the wellness, the fragrances, the skincare etc and the total spend is actually well over €1tn every year. It’s massive.

One example: the Luxury segment in cruises are by far the best performers with 2026 already essentially all sold and 2027 over 1/3 gone already, similarly 5 and 6 star hotels are almost always the star performers in hospitality, it is just another aspect of the K-shaped economy that has materialised almost everywhere.

So when you think of Luxury it’s not just the brands themselves, it’s the entire ecosystem as this ‘daisy’ chart illustrates: at the core is the Luxury customer which is what it’s all about.

And all of this is generated by less than 3% of the world’s population, this was 1% twenty years ago and could well be 5% in ten years’ time (think just of the growing wealth levels in Emerging Markets), the upside is very significant and this is why this remains such an exciting area to invest in.

The Luxury sector evolves all the time and has done so at growing speed in recent years, it’s certainly patchy with not all components working well but with some that absolutely do – the challenge is to stay on top of the trends and surf the right wave because the end prize is a significant one.

// Flavio Cereda-Parini, Investment Director, GAM Investments

Historisk avkastning är ingen garanti för framtida avkastning. En investering i värdepapper/fonder kan både öka och minska i värde och det är inte säkert att du får tillbaka det investerade kapitalet. Avkastningen kan också öka eller minska på grund av förändringar i valutakursen. Vi reserverar oss för eventuella fel i aktie- och fondinformationen som lämnas på denna sida. Åsikter och slutsatser som framkommer i bloggen är skribentens egna och skall inte ses som investeringsråd och/eller åsikter från Avanza.